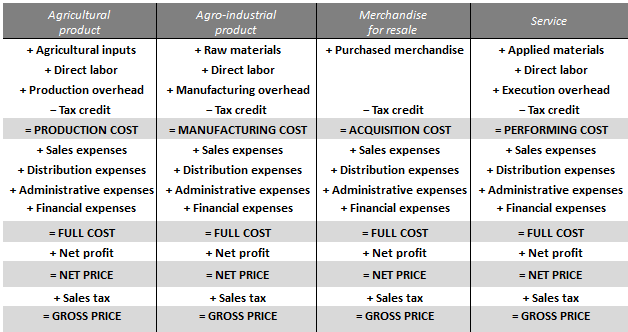

The elements of the cost of a sales object—be it an agricultural commodity, agro-industrial product, merchandise for resale, or service—are usually presented differently from what occurs in accounting reports, as shown in the table below.

Even planting, animal husbandry, and forest exploitation activities can be subject to this cost structure. Even the fact that some operations have an extended production cycle does not prevent them from arranging their elements this way.

There are other manners to demonstrate the cost of a sale object. But, whatever the choice, it is essential to bear in mind, as Nagle, Hogan, and Zale warn in their book The Strategy and Tactics of Pricing: a Guide to Growing More Profitably, that “the best way to avoid being misled by a traditional income statement is to develop a managerial costing system independent of the system used for financial reporting.”

An example of discrepancies between the numbers presented by an accounting report and a management costing report originates from future expenditures. While these expenses are rarely part of accounting statements, they are indispensable in management calculations. This happens with the costs scheduled for the product to manufacture, the freight of CIF merchandise (cost, insurance, and freight included) that has yet to be delivered, and warranty services that still need to be performed.

On the other hand, whether or not to include tax credits and sales tax inside the offer’s cost structure mentioned in the table above will depend on each country’s, region’s, or product’s tax system.

C. L. Eckhard, author of Pricing in Agribusiness: setting and managing prices for better sales margins.

Claudio Luiz Eckhard is a former professor, business consultant, and author of the books “Ajustando o Rumo”[Adjusting the Business Course], “Gestão pela Margem”[Management by Margin], “A Empresa Saudável”[The Healthy Company], and “Pricing no Agribusiness”[Pricing in Agribusiness].

Claudio Luiz Eckhard is a former professor, business consultant, and author of the books “Ajustando o Rumo”[Adjusting the Business Course], “Gestão pela Margem”[Management by Margin], “A Empresa Saudável”[The Healthy Company], and “Pricing no Agribusiness”[Pricing in Agribusiness].